When the Premium Outlasts the Loan

The final car payment cleared three years ago. Your mileage dropped from commuting range to errands and appointments. The comprehensive and collision premiums on your renewal notice read exactly as they did when the vehicle was financed and you drove twice as far. You suspect you're overpaying, but the agent's answer when you asked was vague: "full coverage protects your investment." The car's book value is now $8,500. The annual collision and comprehensive premium together runs close to $900. That ratio doesn't track.

This article walks the actual calculus: what full coverage costs against what it pays when the car is paid off and lightly driven, which Virginia carriers handle mature-driver and low-mileage profiles well, and how the state's discount mandate works when the statute requires the discount but leaves the amount to each insurer's filing.

Compare rates from carriers that specialize in senior drivers

Mature driver discounts, low-mileage rates, and coverage reviews — see what you're actually eligible for.

Get Your Free QuoteVirginia Discount Age Floor

55+

Va. Code §38.2-2217(A) requires insurers to offer a mature-driver discount for operators 55 and older. The statute mandates "an appropriate reduction" but does not fix the percentage: each carrier sets the amount in its rate filing, and you verify yours at quote time.

Va. Code §38.2-2217(A)

What Full Coverage Actually Pays on a Paid-Off Vehicle

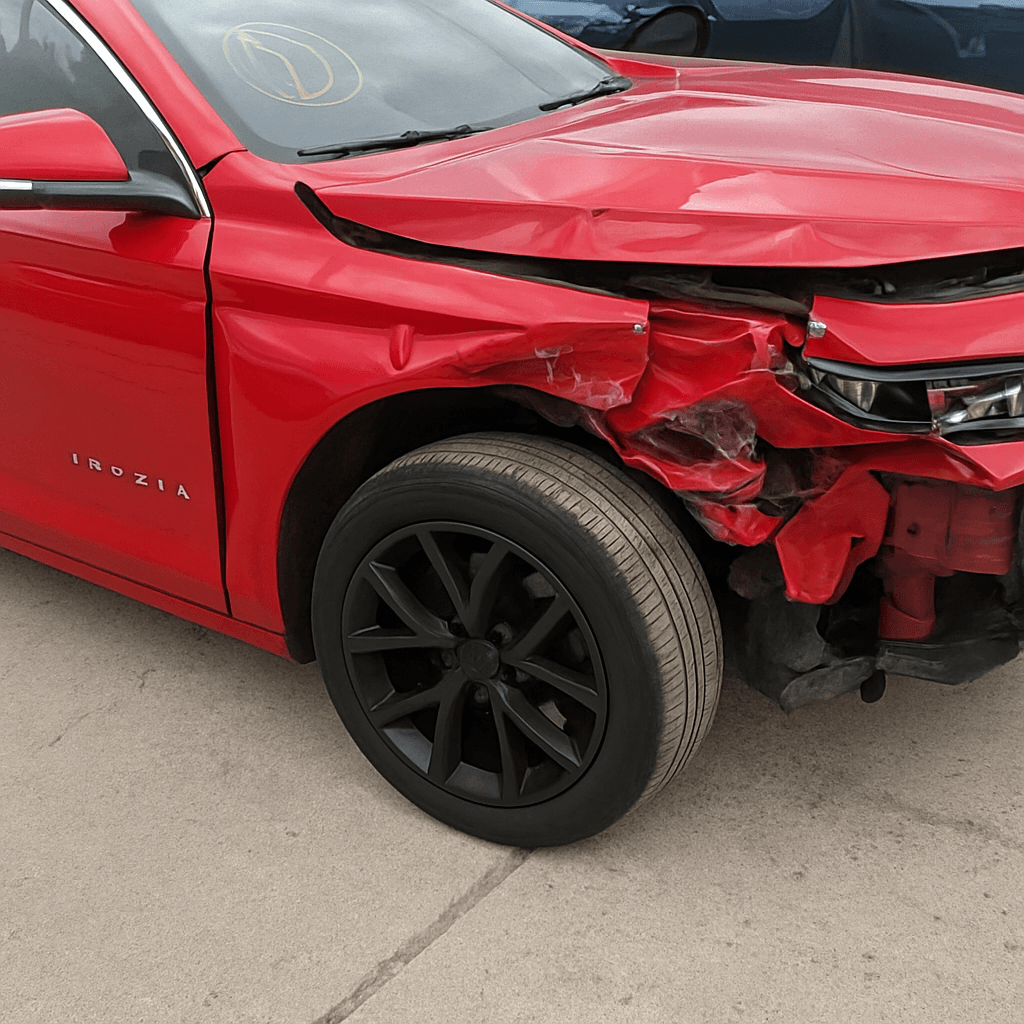

Collision pays repair or actual cash value when you hit another vehicle or object. Comprehensive pays for theft, vandalism, hail, flood, animal strikes, and glass damage. Both operate with a deductible you choose at policy setup, commonly $500 or $1,000. When the car was financed, the lender required both. Now that it's paid off, the lender requirement disappears and you choose based on value and exposure.

The coverage pays up to the car's actual cash value at the time of loss, not replacement cost and not the amount you paid years ago. A 2016 sedan that was $22,000 new may appraise at $8,500 today. If totaled, the carrier pays $8,500 minus your deductible. If the annual premium for collision and comprehensive together approaches 10 to 15 percent of the car's current value, you're paying a significant fraction of what you'd recover in a total-loss scenario every single year. That ratio tightens further as the vehicle ages and premiums hold or rise.

Liability coverage remains mandatory regardless of the car's value or loan status. Virginia's minimum is $50,000 per person and $100,000 per accident for bodily injury, plus $40,000 property damage. Retirees with assets to protect typically carry higher limits, and liability premium does not track to vehicle age. The full-coverage question applies only to collision and comprehensive, never to liability.

The blocker is informational: you cannot resolve whether to keep or drop collision and comprehensive until you know the car's current appraisal value and the exact premium each coverage adds to your bill, itemized.

The Premium-to-Value Decision Frame

Start with the car's actual cash value. Use your insurer's valuation tool if available, or check Kelley Blue Book and NADA for your vehicle's year, make, model, mileage, and condition. The appraisal gives you the maximum payout ceiling before the deductible. If the car appraises at $8,500 and your deductible is $1,000, the net maximum recovery from a total-loss collision claim is $7,500.

Next, isolate the annual premium for collision and comprehensive only. Request an itemized declaration page showing each coverage's cost separately. Add collision and comprehensive together, then divide by the car's current value. If that percentage runs above 10 percent, you're paying a material fraction of the car's worth annually. If it exceeds 15 percent, the coverage may cost more over two or three years than you'd recover in a total loss, depending on claim frequency and deductible.

Related Articles

How Mileage and Profile Affect the Comparison

Virginia carriers writing retiree profiles include State Farm, Geico, Progressive, Nationwide, and Allstate. State Farm and Geico both file FR-44 certificates for DUI suspensions in Virginia and maintain standard-tier programs for clean-record seniors. Progressive and Nationwide offer online quoting and explicitly market low-mileage and usage-based programs that can lower premiums when annual mileage drops below 7,500 miles. None of these carriers publish senior discount percentages publicly: the amount is set in each carrier's rate filing per the statute's mandate, and you verify it at quote time by asking directly.

Low-mileage programs typically require odometer verification or telematics enrollment. If you drive under 7,500 miles annually, ask each carrier whether a mileage tier or usage-based discount applies and how much it reduces the comprehensive and collision premiums specifically. These programs matter most to the coverages priced on exposure: collision and comprehensive track to mileage and theft-risk zip codes, whereas liability pricing leans more heavily on driving record and coverage limits.

Medicare coordinates with medical-payments coverage and personal injury protection differently than employment-era health plans. Medicare Part B covers accident-related medical bills as secondary payer when auto medical payments or PIP exists on the policy. If your policy includes medical payments coverage at $5,000 and Medicare Part B is active, the auto coverage pays first up to its limit, then Medicare covers remaining eligible expenses. Many retirees reduce or drop medical payments once Medicare enrollment is confirmed, but verify coordination rules with both your insurer and Medicare before removing the coverage outright.

The mature-driver discount applies to the entire policy premium, not solely to collision and comprehensive. When comparing carriers, confirm whether each applies the discount automatically at age 55 or requires you to request it. Some insurers apply it at renewal without action; others require you to submit proof of age or complete a state-approved defensive driving course even though the statute does not condition the discount on course completion. Clarify the carrier's specific trigger before assuming the discount is already reflected in your current premium.

State-Specific Discount and Filing Mechanics

Virginia is one of two states requiring FR-44 certificates instead of SR-22 for DUI reinstatement, mandating liability limits of $50,000/$100,000/$40,000 versus the standard SR-22 minimums. This does not apply to clean-record retirees, but it surfaces in carrier availability: insurers filing FR-44 in Virginia tend to maintain broad underwriting appetite across risk profiles, including seniors with standard records. Geico, Progressive, State Farm, Nationwide, and Allstate all file FR-44 here and write clean-record seniors with online or phone quoting.

The mature-driver discount statute requires insurers to offer "an appropriate reduction" for operators 55 and older but does not specify the percentage. Each carrier files its own discount amount with Virginia's Bureau of Insurance. When you request a quote, ask the agent or online tool to confirm whether the mature-driver discount is applied, what percentage it represents, and whether it renews automatically or requires periodic re-verification. If the percentage is not disclosed at quote time, request it in writing before binding coverage.

State-approved defensive driving courses can trigger additional discounts at some carriers, separate from the age-based mature-driver discount the statute mandates. The course-based discount is voluntary, not required by law, and the amount varies by carrier. If you complete a state-approved course, submit the certificate to your insurer and ask whether a course-completion discount applies on top of the age-based discount already mandated. Do not assume the course discount is automatic: most carriers require you to submit the certificate and request the discount explicitly.

Standard-Tier Carriers in VA

6

At least six standard-tier carriers write clean-record seniors in Virginia with online or phone quoting: State Farm, Geico, Progressive, Nationwide, Allstate, and Erie. All file mature-driver discounts per the state mandate; the percentage varies by carrier filing and you verify it at quote time.

Carrier filings, Virginia Bureau of Insurance

When Dropping Coverage Makes Sense and When It Doesn't

Drop collision and comprehensive when the car's value falls low enough that a total-loss payout minus the deductible would not cover replacement, and you have cash reserves to replace the vehicle outright if totaled or stolen. Keep both coverages when the car's value still exceeds $10,000, you lack liquid reserves to replace it, or you park in a high-theft-risk area where comprehensive claims are common. The threshold is not universal: it depends on your risk tolerance, savings position, and whether losing the car would create immediate hardship.

Consider dropping collision only and keeping comprehensive when the car is older but you park outside or in an area with hail, flood, or animal-strike exposure. Comprehensive covers non-collision losses at a lower premium than collision, and those perils do not correlate with mileage. If your annual mileage is under 5,000 and collision premium runs high, removing collision while keeping comprehensive can cut costs meaningfully without leaving you exposed to weather and theft risk.

Raise the deductible before dropping coverage entirely. Increasing the deductible from $500 to $1,000 lowers the collision and comprehensive premiums immediately and keeps the coverage active for severe loss scenarios. If the vehicle appraises at $12,000 and you can afford a $1,000 out-of-pocket expense, the higher deductible preserves coverage against total loss while reducing annual cost. The deductible increase pays for itself in premium savings within one to two policy terms for most retiree profiles.

Compare Carriers and Lock the Fit Decision

Request itemized quotes from at least three Virginia carriers writing retirees: State Farm, Geico, and Progressive are the baseline comparison set. Ask each to quote identical liability limits, then provide two collision and comprehensive scenarios: one with your current deductible and coverages intact, one with collision removed and comprehensive kept at a $1,000 deductible. The side-by-side comparison shows exactly what each coverage costs and what removing it saves. Verify that each quote reflects the mature-driver discount and any mileage-based program you qualify for before comparing total premiums.

Bind the new policy or adjust your current one after you decide, not during the quote process. Switching mid-term can trigger short-rate cancellation fees with your current insurer, and coverage gaps between policies risk license suspension under Virginia's continuous-insurance requirement. Align the effective date of any change with your current policy's renewal date, or confirm that the new carrier will backdate coverage to avoid a lapse. Virginia uses electronic insurance verification: the DMV receives real-time notice of policy cancellations, and a lapse triggers registration suspension quickly.

Once you drop collision or comprehensive, that decision holds until you choose to add it back. Retirees who drop collision and later want to restore it face underwriting review and potentially higher premiums if claims occurred in the interim, even non-collision claims. Make the drop decision with the assumption it is permanent unless the car's value or your financial position changes materially. The coverage you remove today is harder to restore tomorrow at the same rate.